2.20.26 Tredas Weekly Recap

Weekly Action:

Mar26 Corn down 3.75 at $4.28

Mar26 Beans up 5.25 to $11.3825

Mar26 Chi Wheat up 26.25 to $5.75

Mar26 KC Wheat up 31.25 to $5.7375

Mar26 Cotton up 92 points to $0.6303/lb

Feb26 Hogs up $0.025 to $86.975

Feb26 Fats up $3.225 to $246.3

Mar26 Feeders up $1.175 to $367.325

Dec26 Corn up 0.25 to $4.6475

Nov26 Beans up 1.5 to $11.15

July26 Chi Wheat up 31.75 to $5.8875

July26 KC Wheat up 30.75 to $5.98

Dec26 Cotton up 94 points to $0.693/lb

Crop Insurance Price Discovery (as of 2/13) - $4.58 corn & $10.87 beans.

Current 2026 Soybean/Corn Ratio ~2.39

Grains:

Old crop corn continues to struggle to make gains with large ending stocks and open weather allowing everyone to haul grain right now which is keeping end users well supplied and putting pressure on nearby basis. New crop corn has quietly been moving higher and finished the week in line with last week’s highs. Dec’26 futures are within about 6 cents of last years contract highs which were set in February so as we start looking ahead to this year’s crop this would be a good place to consider getting started on your marketing plan if you haven’t already. Ethanol production this week rose to 329 million gallons and continues to be on pace to reach the UDSA’s estimate of 5.6 billon bushels of corn used for ethanol in the 25/26 crop year. Ethanol stocks rose 14 million gallons this week on the increase in production but remain 2.4% below this time last year. US export sales this week were 57.9 million for corn, 29.3 million for beans, and 10.6 million for wheat. Corn and wheat volumes were lower than last week while beans were up and a 3 week high.

The USDA forecast 2026 corn acres yesterday at 94 million and soybeans at 85 million with total crop acres at 224 million which would be down 1.3 million from last year. The official estimate of planting acres will be released in the USDA report on March 31st. The USDA indicated in the outlook forum that they expect corn, soybean, and wheat prices to average 10 cents per bushel better than last year. The current crop price forecast are $4.30 for corn, $5.00 for wheat, and $10.30 for soybeans.

Soybean crush last month came in at 221.6 million bushels which was above market expectations of 218.5 million, and 10.6% higher that last January’s crush. The 25/26 crush rate is 7.2% higher than last year so far and is on pace to reach the USDA annual crush estimate of 2.57 billion bushels which is a 3.5% projected increase from last year. Soy oil futures and in turn soybean futures have been up this week in anticipation of the EPA ruling on RIN allocation for domestic and foreign feedstock and 45z blender credit amounts. A ruling is anticipated in the next 1-2 weeks. The soybean harvest in Mato Grosso Brazil is estimated to have reached 68-70% so far which is about 1.33 billion bushels. An additional 500 million bushels of beans will be harvested in the next 2 weeks as harvest there nears completion. The Safrina corn seeding is estimated to be near 70% complete as it follows soybean harvest.

Wheat has rallied about 34 cents this week and has pushed up to initial chart resistance levels at $5.75 on old crop and $5.85 on new crop futures. Cold weather in the US again after a warm week and French wheat conditions declining 3% due to heavy rains may have contributed to this but at this point it appears mostly technical driven with funds holding large short positions headed into spring where prices seasonally tend to improve. The next chart resistance level to watch for is at $6 futures.

The US Supreme Court has ruled this morning that President Trump’s use of tariffs under the Emergency Economic Powers Act did not meet the use as a national emergency and therefore are not lawful. The court struck down the use of tariffs by a vote of 6-3. How this ruling with affect the current tariffs is yet to be seen but billions of dollars already paid in tariffs may need to be refunded. President Trump in his press conference today following the ruling said he plans to impose a new 10% global tariff under a different authority.

Livestock:

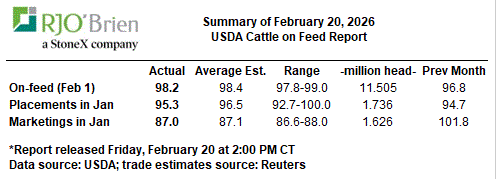

The UDSA released it’s Cattle on Feed report this afternoon and as expected supplies remain tight. Attached is a summary from RJO.

Weather:

South American weather remains ideal for crop growth with rain and moderate temps in the 80’s. The soybean crop is being harvested in Brazil and nearly finished growing in Argentina so the weather focus is shifting to the second corn crop being planted now. The US weather has been warm but is shifting back cooler. Winter wheat is the only crop with any concern on possible winter kill right now. Focus will be shifting to the US in the coming weeks as spring arrives and we get closer to planting.

Economy:

US gross domestic product rose at an annualized rate of just 1.4% according to the Commerce Department which was well below the Down Jones estimate for a 2.5% gain, while inflation in December increased by 3%. It’s estimated that the government shutdown took about 1 percent off of economic growth. For the full year 2025 the US economy grew at 2.2%, down from 2.8% in 2024. The stock market is higher today following the

Nearly 25% of student loan borrower with a payment due are now behind, compared with 9% in 2019. Around 7.9 million student loan borrowers became delinquent in 2025. About 42 million American’s hold student loans with outstanding debt in excess of $1.6 trillion.

President Trump is considering a military strike against Iran if they don’t agree to end their nuclear program. He stated the have at most 15 days to reach a deal before the strikes would begin. Crude oil prices have risen 5% this week in response.

Something That Probably Means Nothing:

The Baltic Dry Index, a measure of global shipping costs for raw materials like iron ore and coal, has quietly hit a 3-month low this week.

Quote of the Week:

In the middle of difficulty lies opportunity - Albert Einstein

Have a great weekend!