2.6.26 Tredas Weekly Recap

Weekly Action:

Mar26 Corn up 2 to $4.3025

Mar26 Beans up 51 to $11.1525

Mar26 Chi Wheat up 10.5 to $5.49

Mar26 KC Wheat down 14 at $5.3125

Mar26 Cotton down 211 points at $0.6106/lb

Feb26 Hogs up $0.125 to $87.375

Feb26 Fats up $1.9 to $237.75

Mar26 Feeders up $7.15 to $367.425

Dec26 Corn up 1.25 to $4.5775

Nov26 Beans up 14.25 to $10.94

July26 Chi Wheat down 6.5 at $5.5

July26 KC Wheat down 10.5 at $5.5725

Dec26 Cotton down 115 points at $0.676/lb

Grains:

Grains traded in a choppy range this week, starting with broad pressure from a risk-off tone in commodities, a firmer dollar, and lingering bearish sentiment from January’s higher USDA ending stocks estimate. Mid-week momentum shifted bullish, particularly in soybeans, on renewed optimism around U.S.-China trade discussions (including social media comments suggesting potential for stronger soybean purchases). Corn held steady to slightly lower amid solid export commitments but faced competition from fast-moving South American harvests. Wheat was mixed, with export sales supportive but macro headwinds capping gains. For producers, the week reinforced the value of monitoring policy tailwinds like the new 45Z guidance while preparing for Tuesday’s February WASDE, analysts expect modest adjustments to exports/ethanol use, potentially tightening stocks if demand surprises higher. This week, soybeans stole the show with sharp gains, while the rest remain range-bound in an oversupplied environment.

On Wednesday, President Trump's post on Truth Social propelled the soybeans nearly 50c higher before settling the day up 25c. We saw similar action today (Friday) with March beans up 20c before closing the day only up 2c. The moral of that story is that rallies are being sold aggressively by other participants. Overall trade volumes exploded Wednesday and set records on the board.

Proposed 45Z Clean Fuel Production Tax Credit: Provides a per-gallon incentive (typically $0.20-$1.00 base, adjusted for emissions performance and prevailing wage/apprenticeship compliance) to domestic producers of low-carbon transportation fuels, including conventional ethanol, biodiesel, renewable diesel, and sustainable aviation fuels (SAF). The credit value scales with a fuel’s lifecycle greenhouse gas emissions intensity, rewarding lower-carbon pathways. The U.S. Treasury and IRS released long-awaited proposed regulations in early February 2026, implementing changes from the Inflation Reduction Act (2022) as amended by the One Big Beautiful Bill (2025). Key provisions include extending the credit through December 31, 2029, requiring eligible feedstocks to be sourced exclusively from the U.S., Canada, or Mexico, removing indirect land-use change penalties from emissions calculations (major win for corn ethanol).

Livestock:

Cattle markets experienced a volatile week, starting with strong gains driven by tight supply fundamentals from the recent USDA Cattle Inventory report, which pegged the total herd at 86.2 million head, the smallest since 1951, and a 1% drop in beef cows to 27.6 million. However, uncertainty surrounding a potential union strike at the JBS Greeley plant triggered sharp sell-offs mid-week, though futures rebounded modestly by Friday amid hopes for resolution and steady cash trade. For producers, this underscores ongoing supply constraints supporting higher prices long-term, but short-term risks from packer disruptions could pressure basis and delay marketings. Next week’s focus is the USDA WASDE Report on updated production estimates and any strike developments.

Economy:

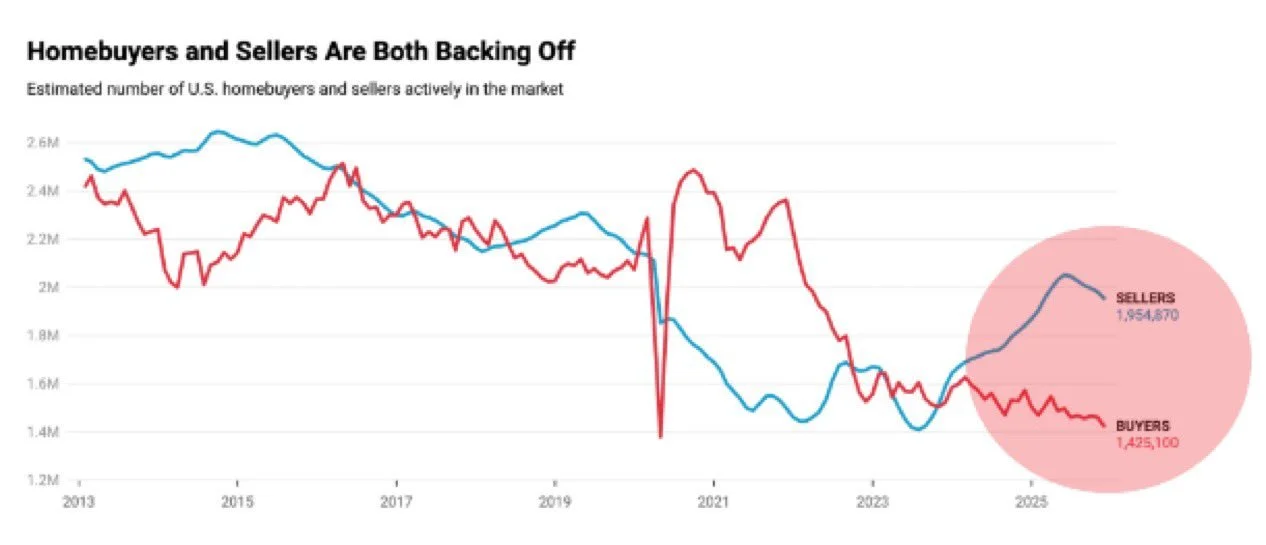

Recent reports reveal a dramatic shift in the U.S. housing market: active home sellers now outnumber potential buyers by approximately 530,000 (with some estimates showing even wider gaps, like 631,000 in December 2025 data). This marks the largest imbalance on record since tracking began in 2013. Both buyers and sellers have been retreating from the market since around 2015 due to high interest rates, affordability challenges, and other pressures. The surge in sellers relative to buyers is creating stronger negotiating power for those still shopping, though it hasn’t yet triggered broad price declines.

Courtesy: Barchart on X

Something That Probably Means Nothing:

A hospital in France had to evacuate after doctors discovered an 8-inch WWI artillery shell in a patient’s backside. It was apparently a “bum-shell” discovery that shut things down for safety. No word on how it got there, but that’s one way to make history repeat itself.

Quote of the Week:

It does not matter how slowly you go as long as you do not stop. - Confucius